November Portfolio Update

+7% in a down market, a new strategy, and the question that's driving my next chapter

Hey friends,

Following the improvements to my trading infrastructure, that I’ve been working on the past few months, we’ve had a pretty solid month of performance

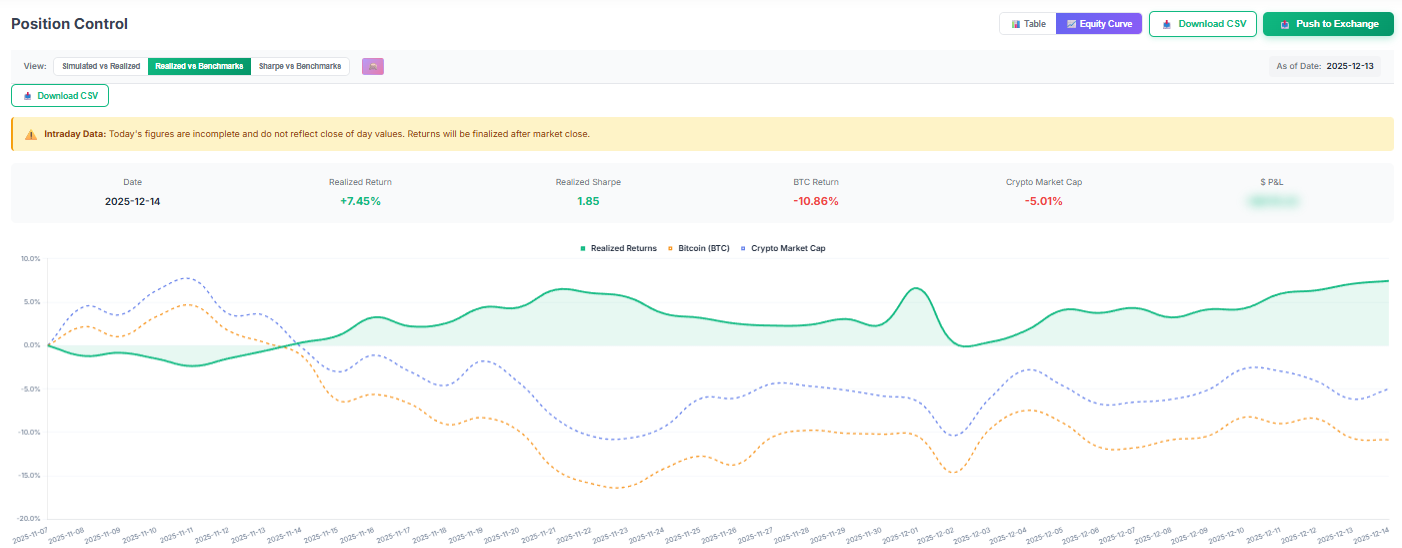

While BTC and altcoins had a pretty rough month, and continue down that trend, the portfolio did quite well and we’re up over 7% from last month.

This is exactly what I am aiming for, and why I’ve devoted the sheer amount of time over the last few months re-designing my entire infrastructure. The goal is to increase sharpe, consistency, and risk management. I will achieve that goal by trading a wider breadth of edges, rather than being focused on just one thing.

On top of the performance above, it’s not yet reflected the performance of a new strategy I’ve deployed, that is a bit non-traditional in the sense that it is a new market. I also wanted to harvest returns right away, so I had to build a temporary external execution engine to be able to trade it. As I am writing this, I’ve already integrated it with my main infrastructure, but at the time I had deployed it, I hadn’t.

I’ve allocated a significant portion of my resources towards that strategy, as it has performed quite above expectations and it’s adding a significant chunk of P&L to my portfolio.

The interesting thing is, I didn’t even have a backtest for it, or any test done.

I took a few heuristics of why it should work, vibe coded an entire execution engine, gave it a few rules, and each morning I began sending the orders through the exchange.

What’s funny about it, is that I thought it was a completely different trade than what it actually became.

Like I said, it’s now a significant contributor to my PnL. A lot of people get stuck in the details and making a backtest perfect, while the market is right there.

What do you think you’ll improve in a backtest that you wont find out live trading it? Even if with small capital. I’ve only discovered this new strategy because I was willing to get to the market quickly, and not spend too much time on the details. Sure, I’ve worked on those details after, and now, I’ve constructed a pretty solid model of the effect I’m harvesting, but I didn’t do it before. I could’ve spent the last 2-3 weeks designing a simulation, not knowing if it would work or not. I’d rather not do that, and get immediate feedback from the market.

But taking risk sucks innit? That’s why most people aren’t willing to go there.

There’s a few characteristics specific to this last strategy that I won’t discuss publicly. I do think there’s some alpha here so I don’t want to get into it too specifically, as you may understand. I do trading as my primary business, and diluting alpha is not a good long-term decision for my business. I am willing to share risk premia strategies and their details, like I’ve done over the last few years on this blog, but not new strategies that are capital constrained.

I’ve also been working a lot on the scalability of the systems. What do I mean by this, more practically? Well, if I design a new model, how long does it take to incorporate it into my main portfolio? Personally, there’s nothing that suggests that I shouldn’t be doing it with a click of a button. It just changes when completely new markets are added, and different execution types are required. But that gets weeded out over time, as we build those tools for individual strategies, and they become part of a well rounded infrastructure.

Indeed achieving that functionality of sending new strategies/features from design phase, to live production, with the “click of a button”.

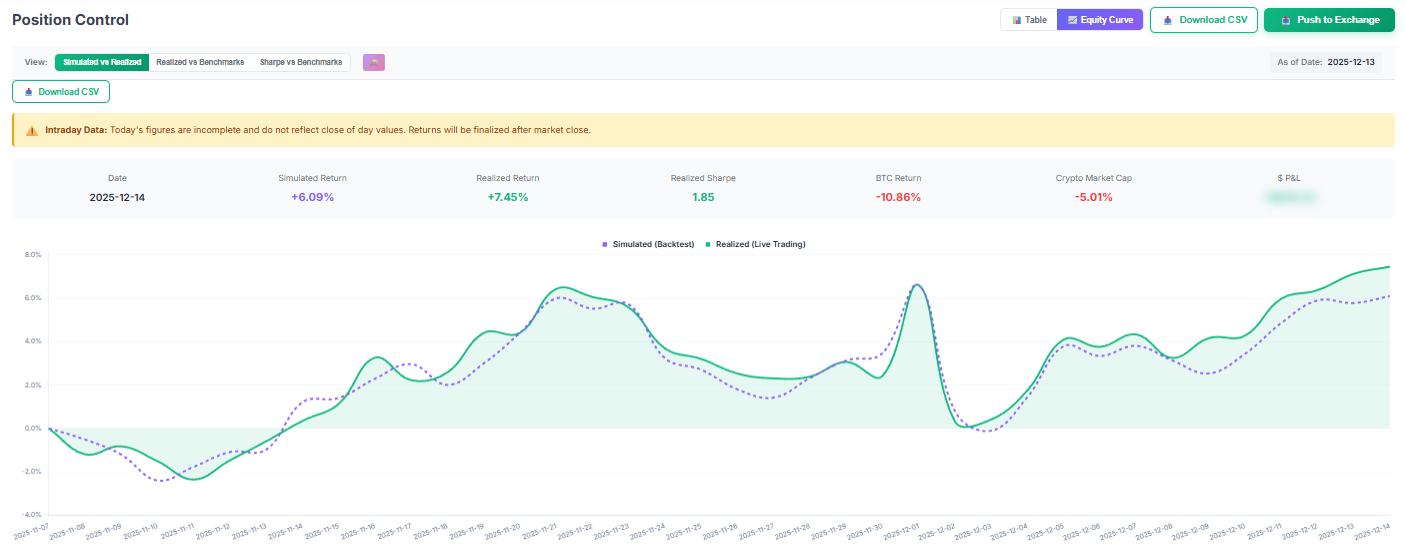

This has another added importance. You always want to ensure that your live trading (green line) matches your simulation (purple line).

To do that you must ensure that the engine that designed the strategy, is the same engine that produces the target exposures.

For example, you can see that I am running at a slightly positive delta to the simulation, and that delta has been broadening a bit over the past few days. You may ask me, why is it? Well, I am going to be very straightforward with you, I am not sure yet. I have few assumptions:

Cost/slippage assumptions on simulation are more aggressive than reality.

The difference in execution time of the live model vs the assumption of the simulation. More specifically, I execute my positions in the morning between 6am-8am, as opposed to the simulation that is set for 00:00 every day.

Compound effects on the calculation of the simulated curve on the backend.

But I don’t yet know for sure as I am writing this, and I’ll have to investigate. My point is that I know I have something to investigate, because I track it. Always make sure that your modeling engine matches your live execution engine!

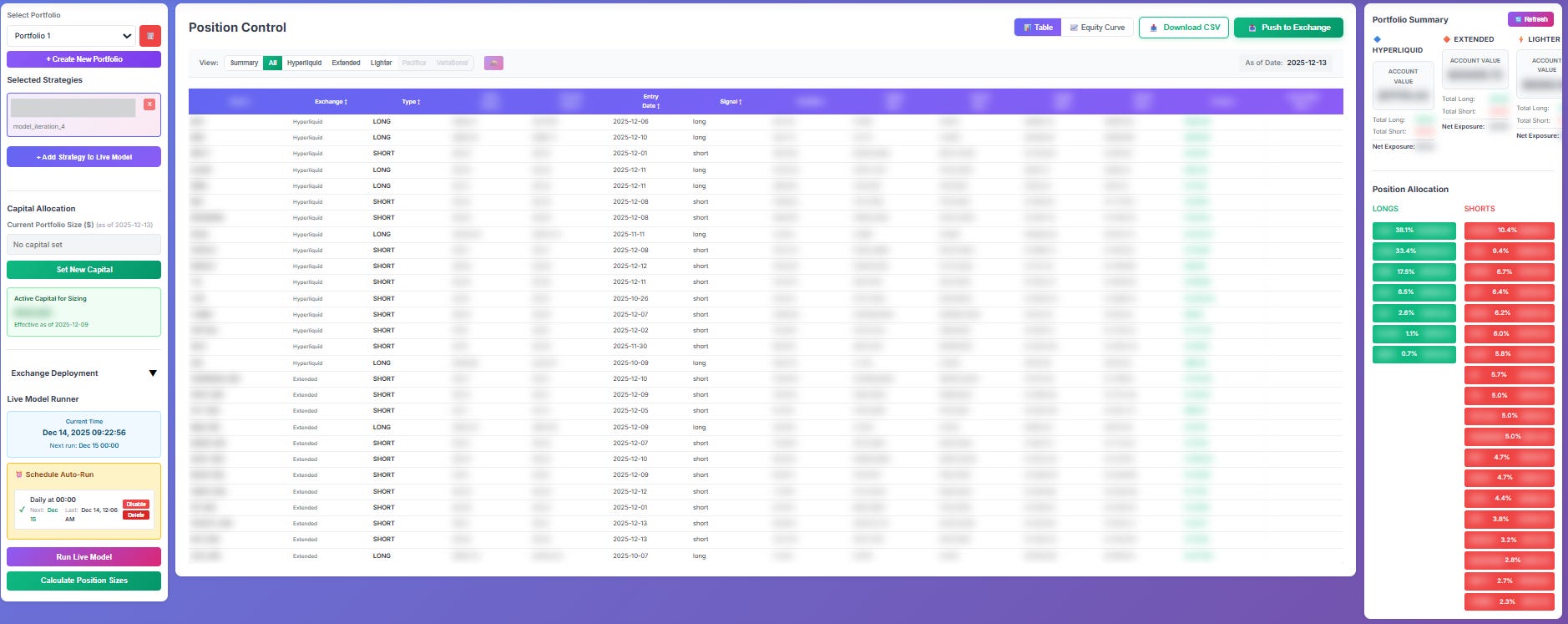

You can see below a table of exposures for the portfolio I so creatively named “Portfolio 1”. This is the portfolio that generated the equity curve at the start of our post today.

One of the most important things I’ve learned when designing trading infrastructure is that I should always be thinking about scalability and future integration. Always think about how scalable this new feature really is given a wide breadth of future edges, and if it isn’t, design it to be. It will save you a ton of time.

This is it for this week. Just wanted to give you this more practical update on the portfolio. It’s doing really well, on par with the expectations I set for it. We’re still scaling the capital that is allocated to it, and as we get more feedback, the more I’ll allocate. I am also designing more strategies that will be launched soon. I have more ideas on the pipeline than I have time to get to.

I am trying to answer the question:

“If I had to purely live off trading gains each month, could I do it?”

Now, that question explicitly excludes savings, external income, etc. Purely “eat what you kill” kind of approach. I am deeply interested by that question at this moment in my career. That means that my sharpe has to be much higher than it is now. It might be a foolish question, because we know different regimes affect strategies in different ways, and no single strategy makes money forever, all the time.

But I want to question that idea…

I personally know people that do it, why shouldn’t I? There’s short/medium-term alphas/edges that we can run that would indeed increase the consistency of PnL on a month to month basis. I know that I can make money over a few months or a year, that is already established, I’ve been doing that for a long time. But my next evolution as a trader/capital allocator will answer this new question practically.

I hope you join along.

Thanks for reading and wish you a great Sunday.

Pedma

Disclaimer: The content and information provided by the Trading Research Hub, including all other materials, are for educational and informational purposes only and should not be considered financial advice or a recommendation to buy or sell any type of security or investment. Always conduct your own research and consult with a licensed financial professional before making any investment decisions. Trading and investing can involve significant risk of loss, and you should understand these risks before making any financial decisions.

What about December?