How a Simple Improvement to Signal Selection Led to 2x the Returns - Research Article #75

Does this trading signal decay with lower constraints?

👋 Hey there, Pedma here! Welcome to the 🔒 exclusive subscriber edition 🔒 of Trading Research Hub’s Newsletter. Each week, I release a new research article with a trading strategy, its code, and much more.

If you’re not a subscriber, here’s what you missed this past month so far:

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

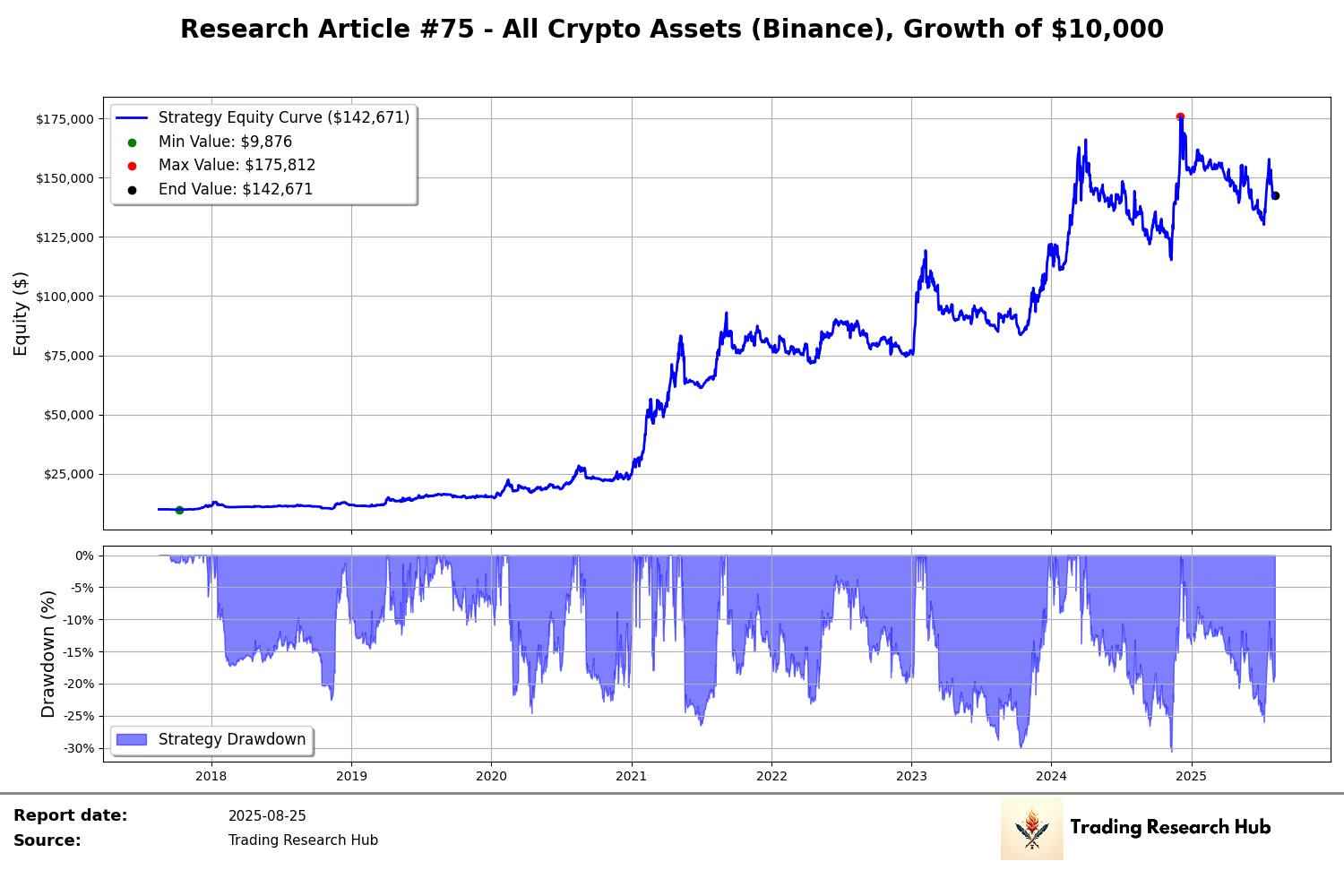

On our last post, we’ve looked at a method that increased the win rate of a simple trend-following strategy from the 30’s%, up to 55%, and even 60% in one of the variations.

However, as I was digging through the data, I realized that the strategy was not allocating capital as optimally as it could. What do I mean? Well, imagine that you have a bunch of signals, and, for whatever reason, you only allocate capital to a very small subset of them, despite the remaining signals being equally profitable. Yes, there’s strategies where the amount of edge that each signal carries, can vary by different thresholds, and some may not even be profitable enough after costs, and we wouldn’t want to take them. But that’s a topic for another article.

By letting go of this constraint, this resulted in a 2x the absolute return performance we had on research article #74:

Mind you, I don’t like optimizations at all, so this wasn’t me optimizing parameters or picking the best performer. It was a simple matter of being more efficient on signal selection.

In trend-following strategies, a common approach is to take all valid signals, but only on “inflection points”.

What’s an inflection point?

Imagine that you’re buying 20-day high breakouts and selling 20-day low breakdowns. A common and simple trend-following signal.

This is fine if you’re trading a small fixed number of assets and you generally have risk budget for all signals that present to you.