The Low-of-Day Stop Loss Rule - Research Article #76

Testing whether observations from swing traders can improve systematic crypto strategies.

👋 Hey there, Pedma here! Welcome to the 🔒 exclusive subscriber edition 🔒 of Trading Research Hub’s Newsletter. Each week, I release a new research article with a trading strategy, its code, and much more.

If you’re not a subscriber, here’s what you missed this past month so far:

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

I spend a lot of time on X (formerly known as twitter). Why? Well, there’s a lot of good stuff in there, if you curate your feed well enough. If I spent that time on pure entertainment, or doom scrolling the “for you” page, then I’d argue it’s time wasted, even though I do it sometimes.

But over the years, being deep in the niche of systematic trading, it has shaped a lot of my thinking to how I trade today. I’ve curated my feed so that I mostly get observations from actual practitioners, that provide me with useful information for my research process.

Even if you tried, you can’t observe every little aspect of market behavior yourself. To solve this, you can either hire an army of researchers, that are working on this stuff for you all day (expensive), or go into the places where people with experience participate in sharing their observations. That’s why I am on X most of the times and also why I write these articles.

I store all of the ideas I find in an organized notion database, where I rank them by different attributes, that I consider important of that particular piece of research. Right now, I have 177 ideas I want to research, and that pipeline is growing faster than I can close them.

Anyways I just wanted to share this because a lot of people ask me how I find ideas to work on. The answer is simple. Be online a lot, read a lot, curate the people that you want to research from, that you think are actual traders, and learn everything you can from them.

That’s what I’ve been doing as I’ve been spending a lot of time digging through the content of discretionary and quasi-systematic momentum traders.

I have this hypothesis that a lot of what these traders observe in the market, is actually important information, and if we can gather some data around it and find out if their observations yield value, we can improve our own models.

As I was exploring a different topic this week, I stumbled across the idea of how different stop-losses affect trading strategies in crypto, particularly trend-following strategies which is what I tend to focus my time on.

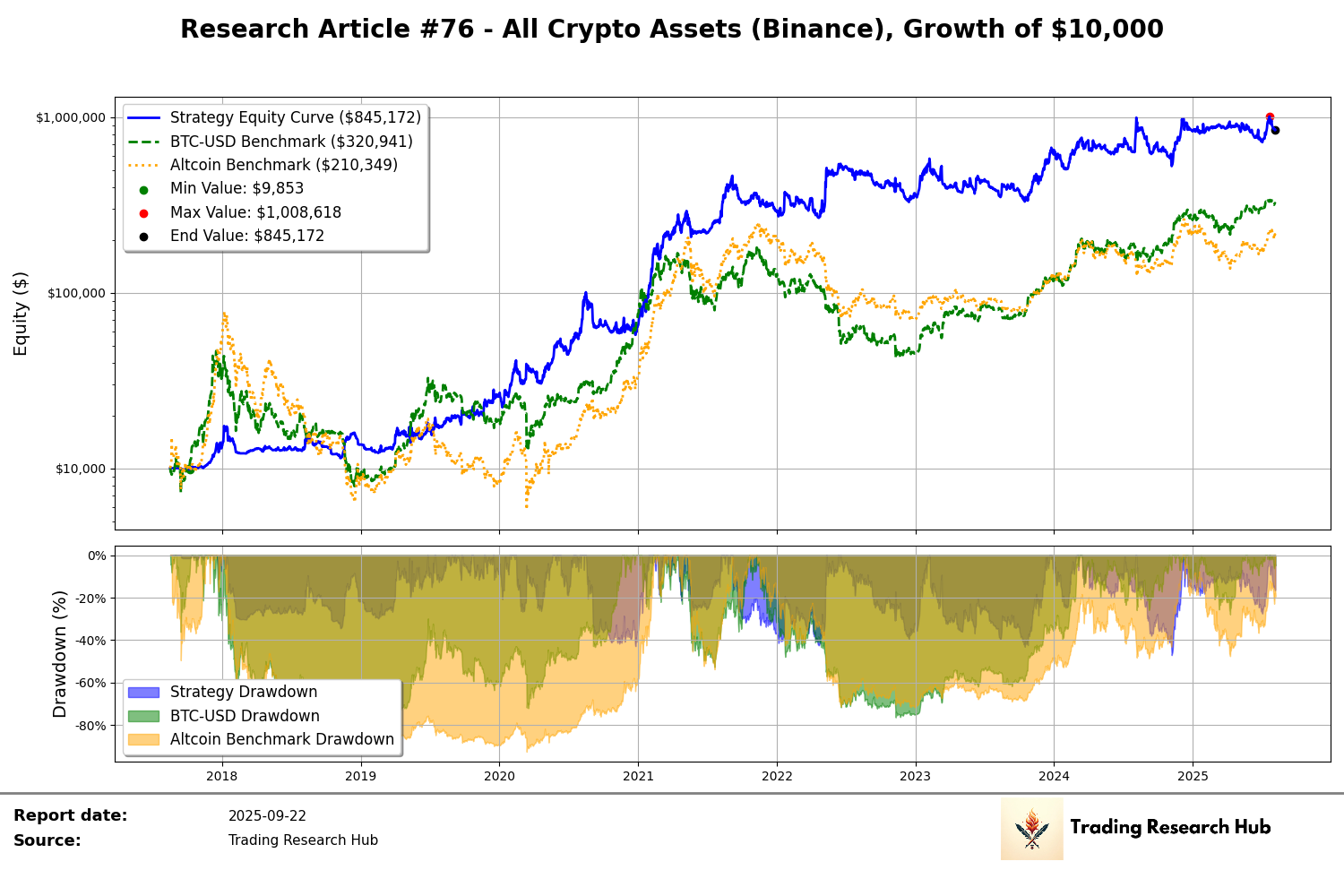

The performance you see below, is what we have achieved by the end of today’s article. The idea was once again obtained via the observation of good quasi-systematic traders I know on X.

Quite cool isn’t it? In trend/momentum world, this is a super neat equity curve. We’re used to much bumpier rides than this.

The idea that we will explore today is around how tighter stop-losses behave in comparison to looser stop losses with an interesting twist by the end of today’s article.