Sector Caps in Crypto — Do They Actually Help?

74% of my losses came from one sector. Can we fix it?

Hey there, Pedma here! Welcome to this ✨ free edition ✨ of the Trading Research Hub’s Newsletter. Each week, I’ll share with you a blend of market research, personal trading experiences, and practical strategies.

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

Hey friends,

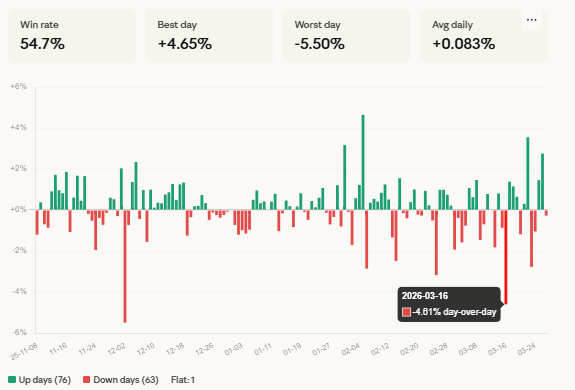

Last week, on the 16th of March, I woke up, did my usual morning portfolio check, and saw a -6% loss on the portfolio, staring back at me.

My first instinct? Exchange bug. Sometimes wallets don’t read capital correctly, happens. I refreshed. Still -6%. Day ended slightly better, below -5%, but the damage was done.

So what happened? Memecoins happened.

“Risk Neutral” — but not really

My portfolio runs a net-neutral approach. Long and short in volatility-weighted amounts, so in theory, I’m not making big directional bets.

I say “risk neutral” very loosely though. Because we’re only neutralizing volatility. Not all risks are mitigated.

When I broke down the major losses that day, there’s exactly one thing they all have in common…

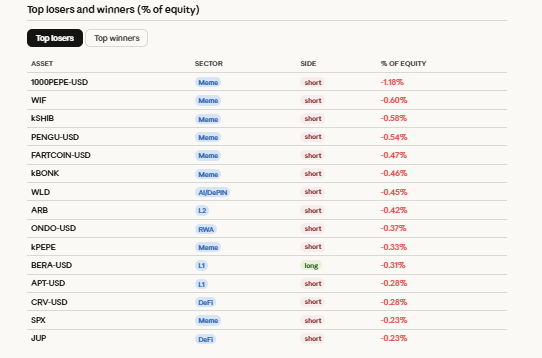

Memecoins.

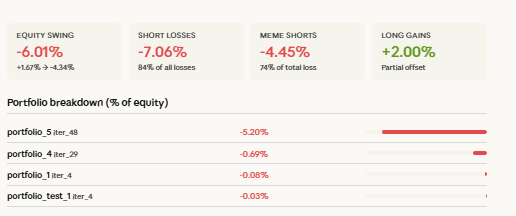

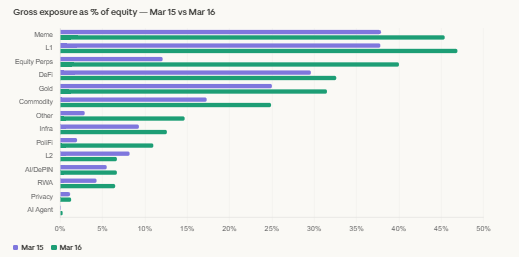

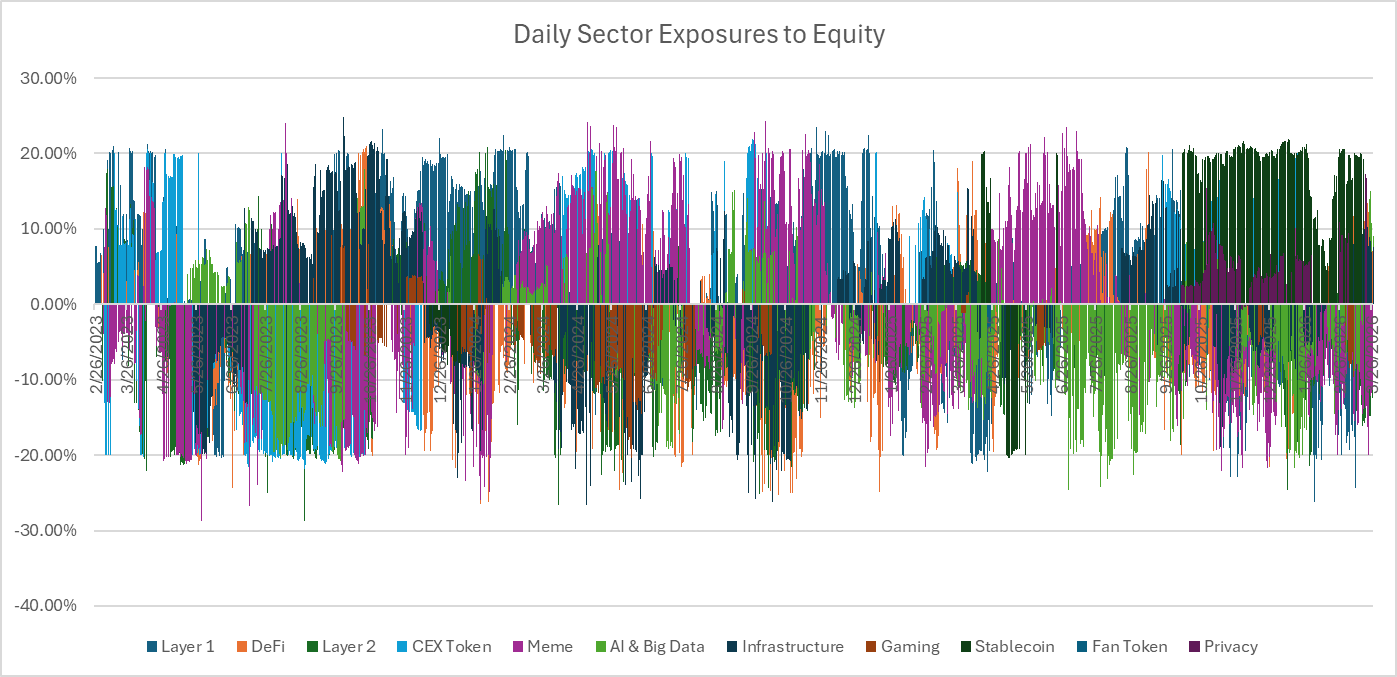

74% of all losses that day came from memecoin exposure. Just that one sector. And when I checked the gross allocation, memecoins accounted for over 45% of total exposure that morning.

Imagine having close to half your portfolio in a single sector. On a day where that sector implodes together.

So what do we do about it?

The idea isn’t complicated. Set sector caps so you never have too much gross exposure to any single sector.

This is the same logic we apply to individual positions. You wouldn’t put 20% of capital into a single name (in most cases). So why let sector exposure run wild when clearly some sectors carry more tail risk than others?

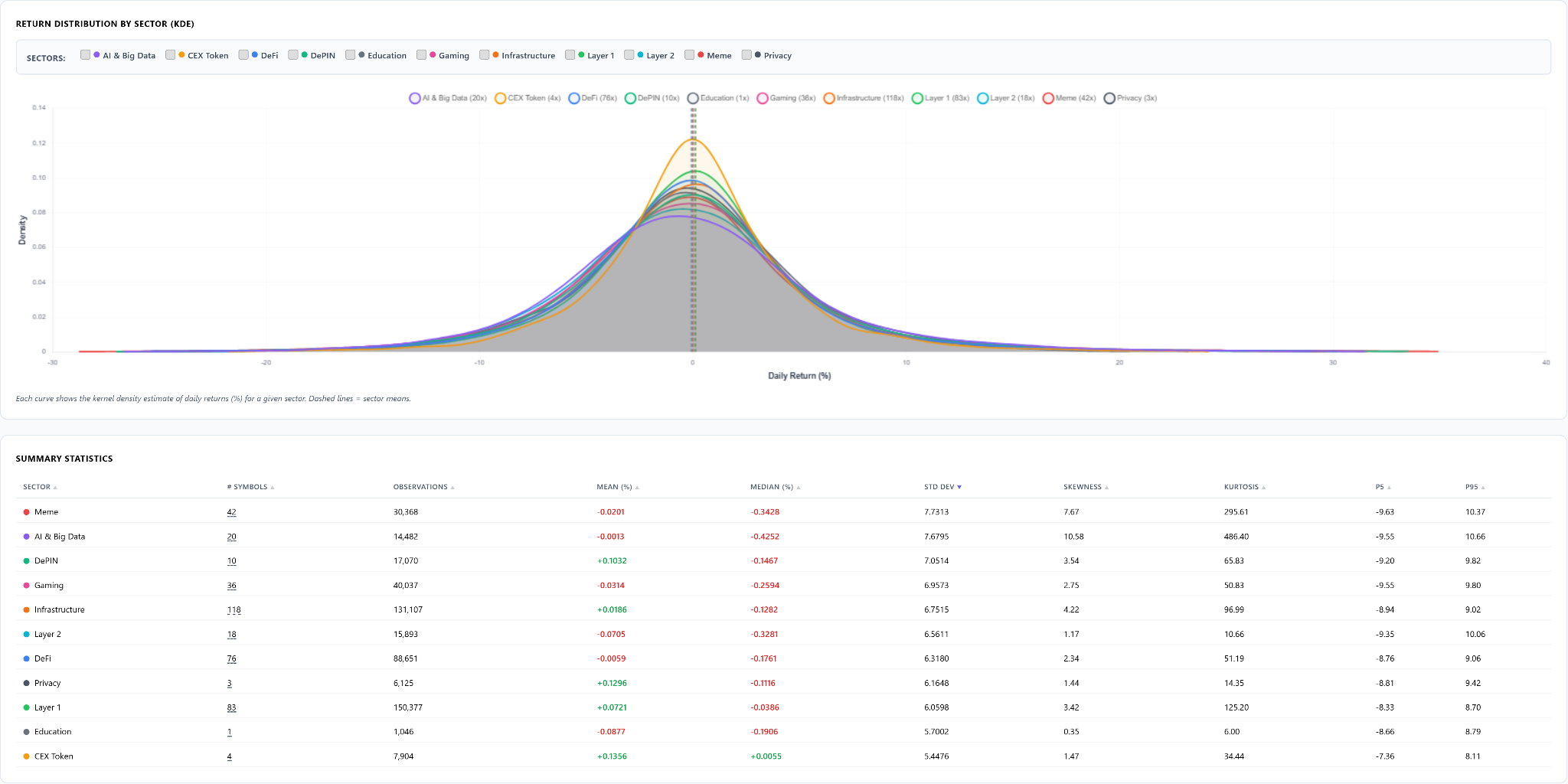

The sector tail analysis confirms this pretty clearly. Memecoins and AI have the fattest tails of the lot — the distributions have long right and left extremes, which means the possibility of truly violent days is higher in these sectors than anywhere else.

Now, I want to be clear about one thing. I am not saying we should pick and choose which sectors to trade. That would be discretionary garbage layered on top of a systematic model. What I’m saying is capping how much exposure we ever take to a single sector seems like a reasonable, rules-based constraint — the same way position size limits are reasonable.

I also wouldn’t go optimizing the cap levels based on historical sector volatility. That’s an overfit waiting to happen. Sector dynamics shift. Keep it simple.

So let’s just test it and see what the data says.

The Tests

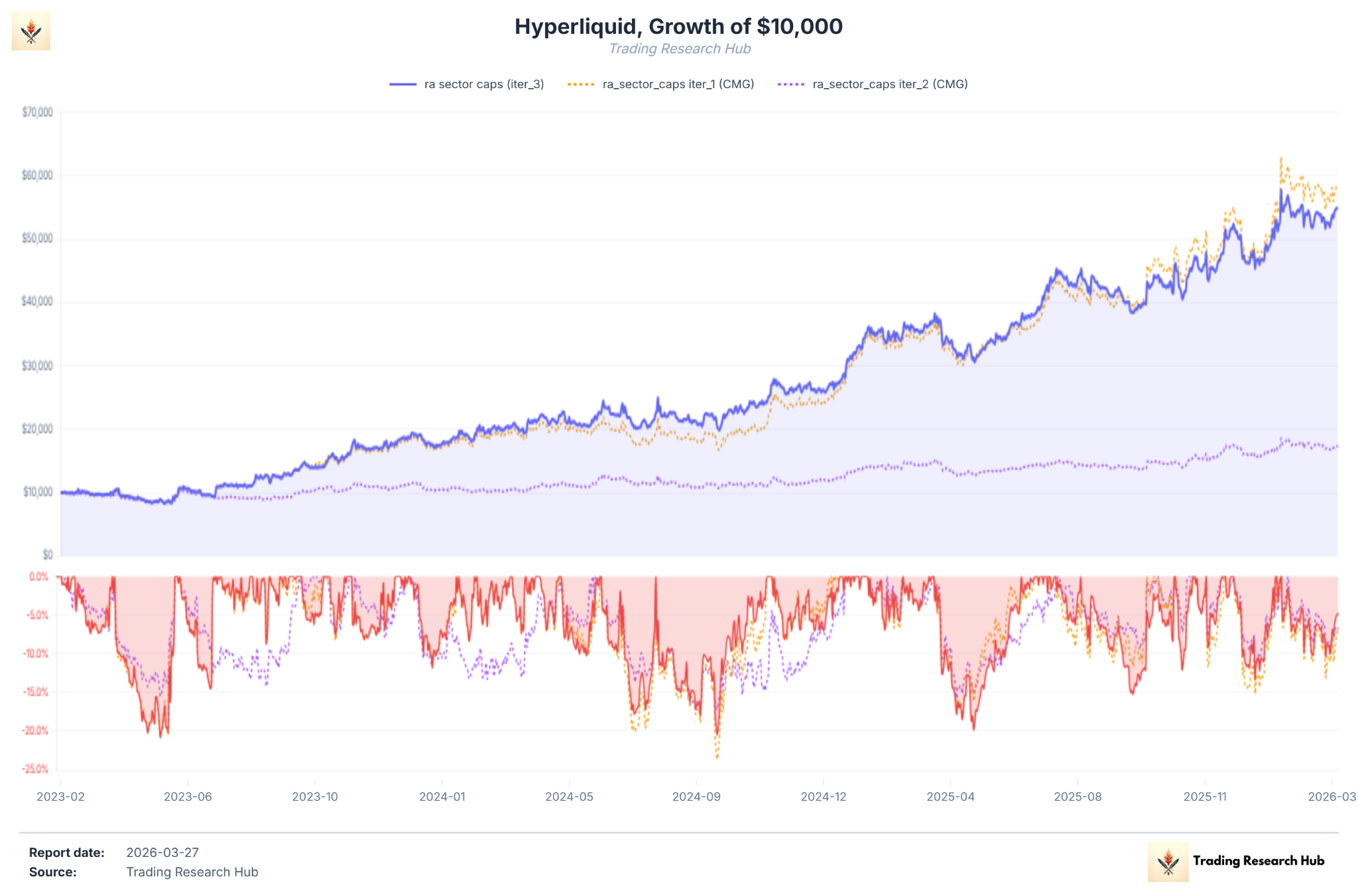

I ran three configurations on Hyperliquid perps:

Iteration 1 — baseline (no caps), my current live system

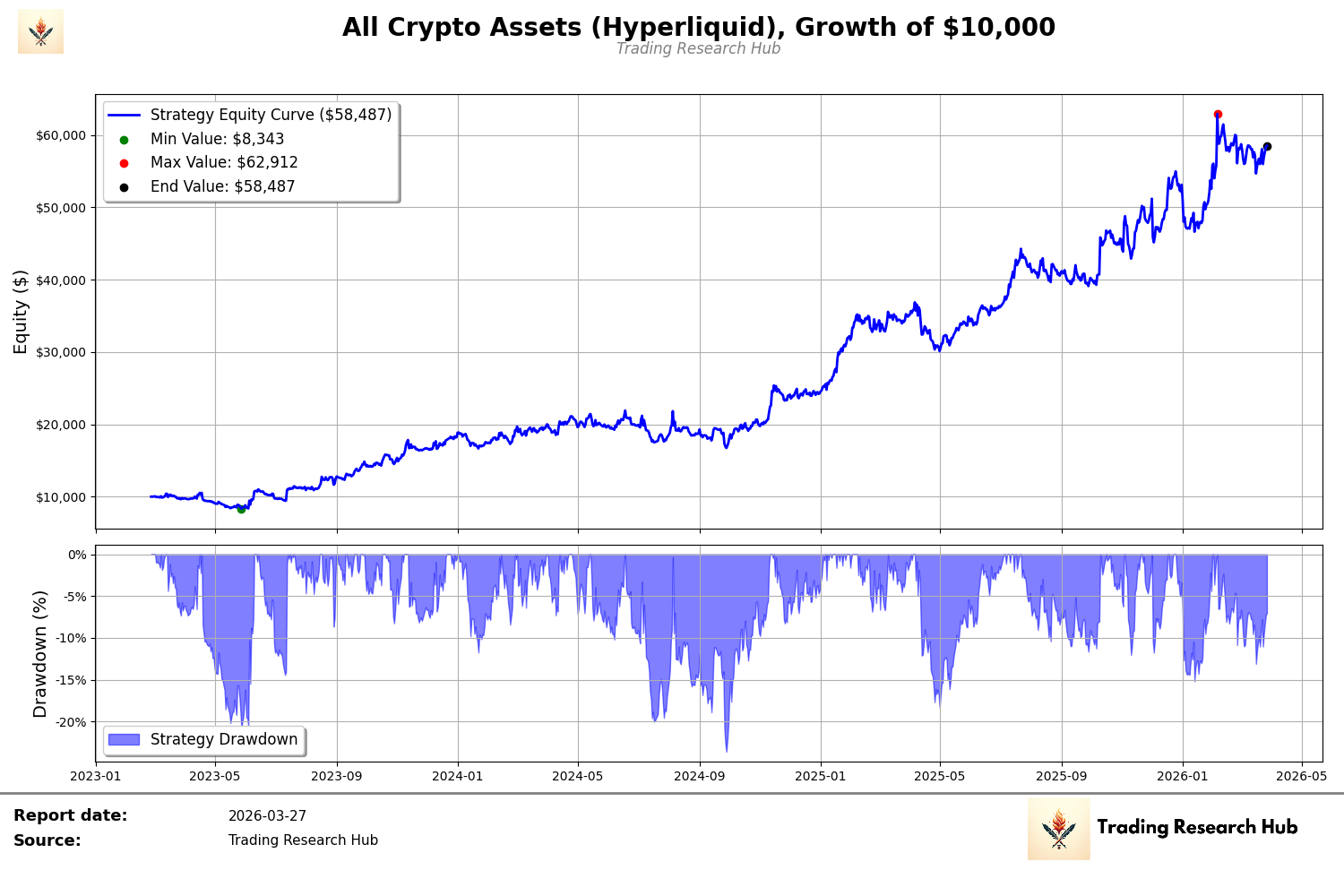

Iteration 2 — 20% cap on all sectors (both sides)

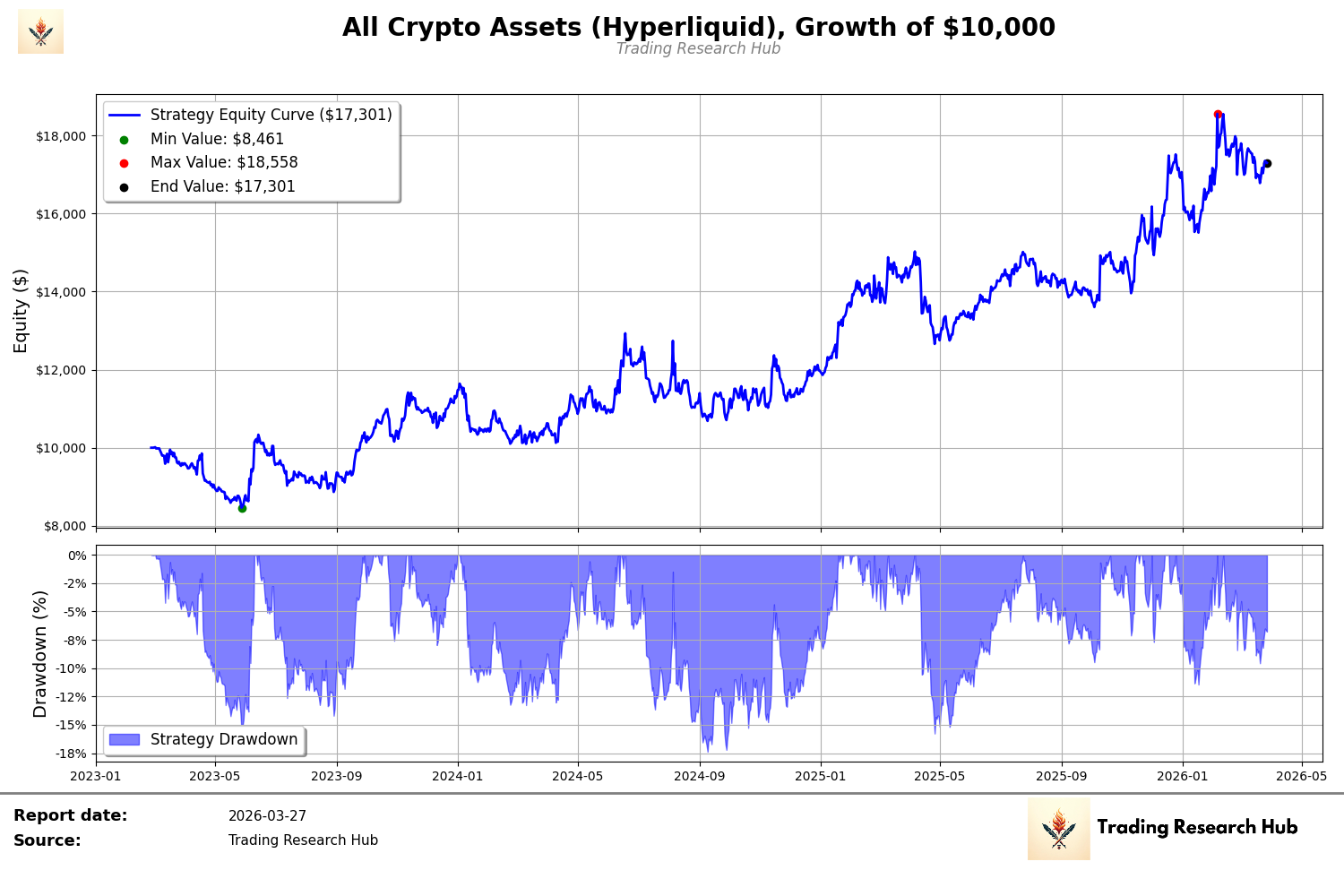

Iteration 3 — 20% cap on Meme sector only (short side)

Baseline — what I’m running now

First, the benchmark. No sector caps. This is the system live in production.

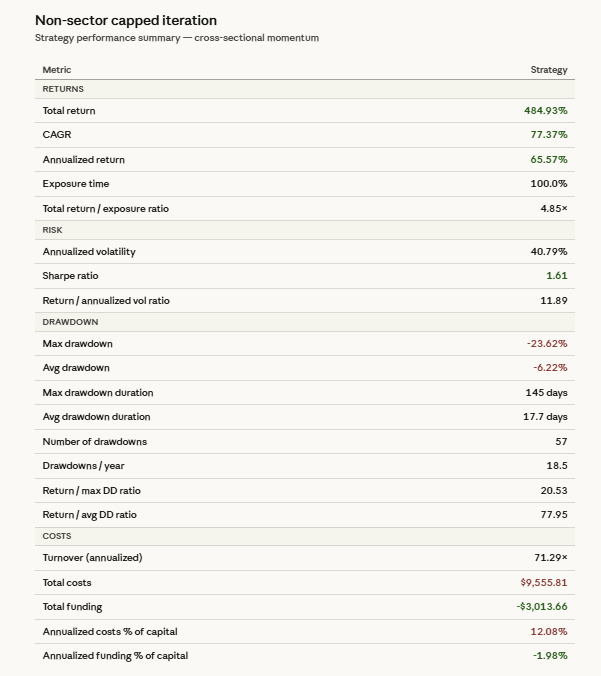

CAGR of 77.4%, Sharpe of 1.61. Max drawdown -23.6%.

20% cap on all sectors — ouch

Now let’s see what happens when we cap every sector at 20% of capital.

The performance gets a massive downgrade.

CAGR drops from 77.4% to 19.5% — a -75% relative hit. Sharpe falls from 1.61 to 0.81. And while volatility compresses from 40.8% to 26.3%, the return compression is disproportionately worse. Worst of all, max DD duration worsened from 145 days to 223 days. So you’re taking less risk but spending more time underwater. Not the deal you’re looking for.

Is that surprising? Tbh, a bit. But when you think about it, it makes sense. In crypto, returns are heavily concentrated in sector rotations. When a sector is running, the edge is in riding it. By capping how much you can be in each sector, you’re basically forcing the model to spread capital into weaker bets.

It’s like saying, in equities, that a large chunk of returns came from the tech sector. Is that wrong? I don’t think so. That’s just where the momentum was.

Let’s at least do a sanity check on the backtest before moving on — always do sanity checks.

Good. The mechanism works correctly. Every time a sector goes above 20%, it gets rebalanced back to target. The plumbing is clean.

20% cap on Meme sector only — interesting

Now the more surgical version: cap only the Meme sector, on the short side.

Performance barely moves.

CAGR: 73.8% vs baseline 77.4% — only -4.6% relative. Sharpe actually ticks up slightly, from 1.61 to 1.63. Max DD improves from -23.6% to -20.8%, and max DD duration compresses significantly — from 145 days down to 97 days.

This is the best risk-adjusted result of the three.

Surgical precision beats a blanket rule. The Meme-only cap shaves a small amount of return while actually cleaning up the drawdown profile. The day I described at the start? That cap would’ve saved a chunk of it.

Putting them all together

The baseline is the historical winner. Meme-only cap is close. All-sector cap is not a competition.

Honestly, the gap between baseline and Meme-only is small enough that I don’t particularly care which one to run. If the delta isn’t large, I’d rather stick with the simplest version. Occam’s razor and all that.

Binance confirms it

This is still a limited dataset. Hyperliquid only goes back to early 2023. So let’s run the same sequence on Binance spot, where history goes back to late 2017.

Iteration 4 — Binance baseline (no caps)

Iteration 5 — 20% cap on all sectors (both sides)

Iteration 6 — 20% cap on Meme sector, short side only

Same pattern. Baseline wins. Other iterations lag.

The all-sector cap drops CAGR from 52.0% to 8.9% — that’s -83% relative, even worse than on Hyperliquid. Sharpe collapses from 1.22 to 0.45. Max DD duration goes from 487 days to 1,502 days — over 4 years spent in drawdown. The strategy was barely trading.

The Binance meme short-only cap holds up much better: CAGR 48.8% vs 52.0%, Sharpe 1.18 vs 1.22. The damage is minimal.

Why does capping all sectors hurt so much? Theory time — though I’ll be honest, I could be totally wrong here.

In crypto, returns are heavily driven by sector rotations. When momentum is running in a sector, that’s where the edge concentrates. A blanket cap forces the model to cut the winners and spread into the laggards. In a trend-following framework, that’s basically the opposite of what you want to do.

The Meme short-only cap is a different story. That’s a pure risk constraint, not a return bet. You’re saying: I don’t want to run heavily short a sector that’s structurally driven by speculation and narrative. That’s reasonable. And the data shows it costs almost nothing in returns.

What I’m taking from this

Blanket sector caps are not the way to go. The momentum strategy’s alpha comes from concentrating in sectors where trends are strongest — cap everything uniformly and you’re killing the engine.

Surgical caps, targeting only the most volatile or structurally weird sectors (memes), are nearly free. Small CAGR cost, cleaner drawdown, and you avoid the kind of morning I described at the start.

For now? I’m keeping things simple. The baseline version is what I run. But if I were to add any constraint, the Meme-only cap is the obvious candidate — it’s the closest thing to a free lunch this analysis produced.

Disclaimer: The content and information provided by the Trading Research Hub, including all other materials, are for educational and informational purposes only and should not be considered financial advice or a recommendation to buy or sell any type of security or investment. Always conduct your own research and consult with a licensed financial professional before making any investment decisions. Trading and investing can involve significant risk of loss, and you should understand these risks before making any financial decisions.