Why Is the WTIOIL Contract on Hyperliquid Paying -400% Funding?

A quick explainer on contract rolls, backwardation, and why a simple arb doesn't actually work

Hey there, Pedma here! Welcome to this ✨ free edition ✨ of the Trading Research Hub’s Newsletter. Each week, I’ll share with you a blend of market research, personal trading experiences, and practical strategies.

If you’re not yet a part of our community, subscribe to stay updated with these more of these posts, and to access all our content.

Hey friends,

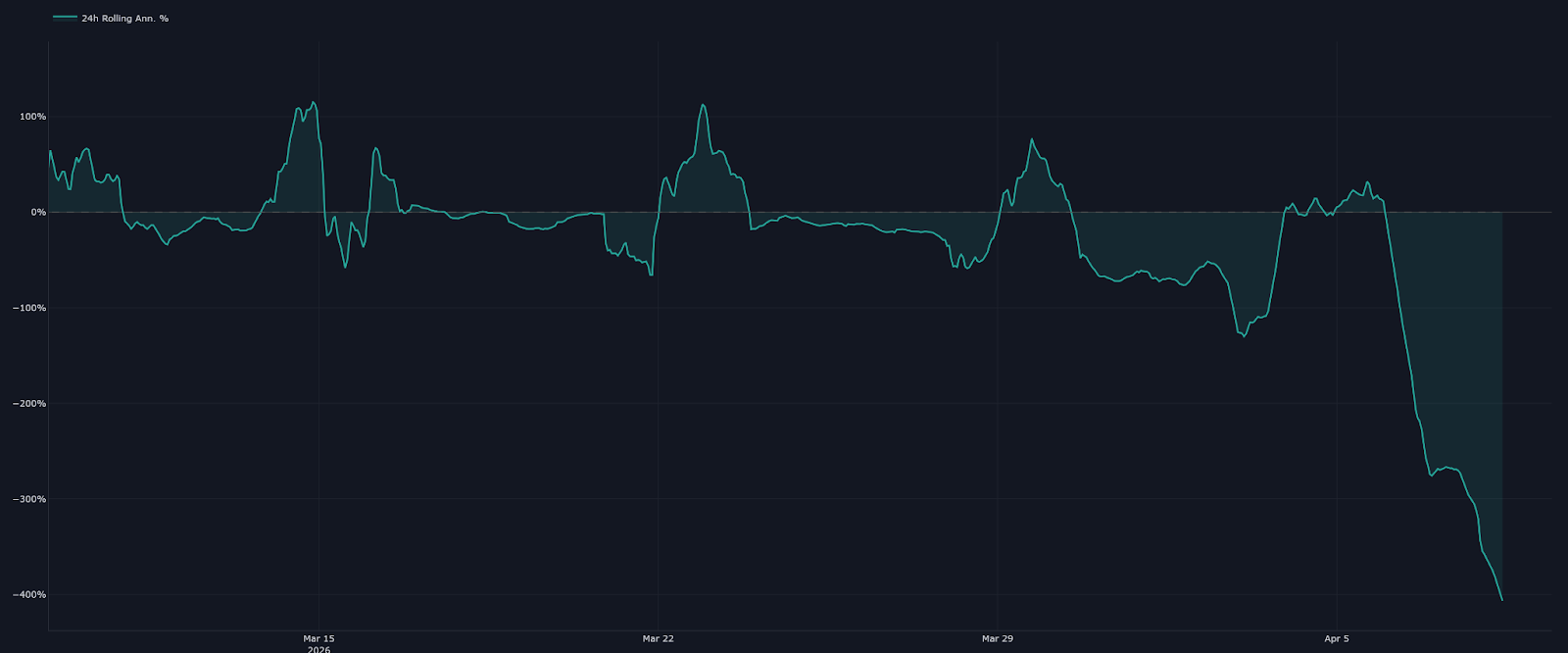

For the past few days the WTIOIL-USDC contract on hyperliquid has been paying between 200%-400% (the annualizoor enters the room) to everyone that is willing to long this thing.

That is about 1.1% each day, just to be long.

The question is , why?

Also is it that easy to make money off of it?

I am going to be straightforward and say that these are not the markets I trade or think about often, so if you see something wrong, please tell me, so I can move forward with better information. This will be my attempt to understand these insane funding readings over the last few days on the WTIOIL-USDC contract on hyperliquid.

So let’s start going down the line of reasoning of why this is happening.

The WTIOIL-USDC contract on Hyperliquid tracks the price of the front-month WTI futures contract which is the nearest-expiry oil delivery contract on the CME. Think of the oil futures market as a chain of monthly contracts, each representing a barrel delivered at a specific date:

May delivery

June delivery

July delivery

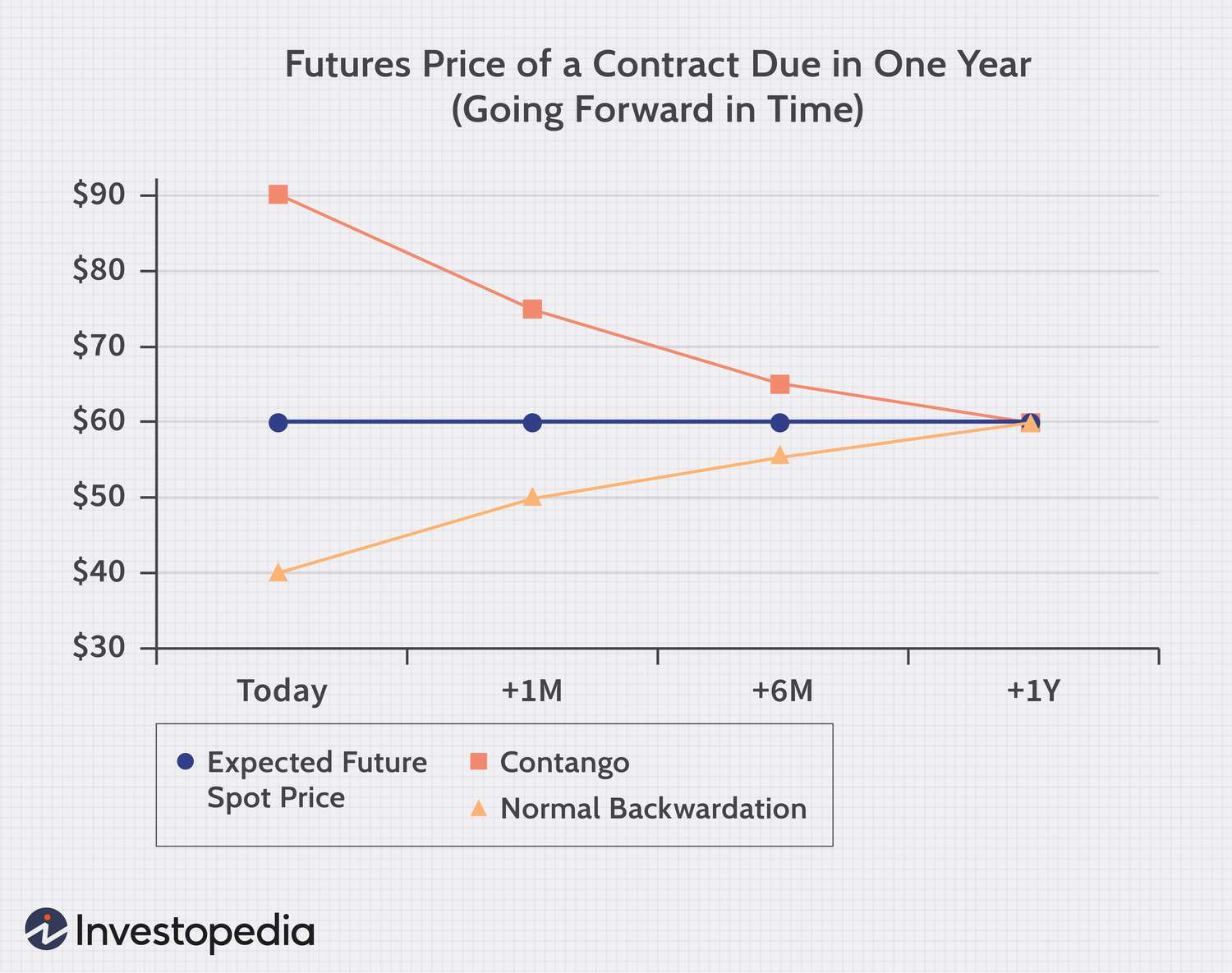

And the relationship between these contracts is described as either in contango or backwardation.

What is contango if not a different breed of an orangotango? (sry about the dad joke)

Well imagine you’re a Saudi producer and I want to buy oil from you.

I say I want 1,000 barrels delivered and you tell me the price is $60 per barrel.

But I want delivery in 6 months.

So you tell me, well, that’s $62 a barrel.

Why are you charging me more though? Because you have costs if you’re committing to that future delivery, like storage, insurance, and financing the inventory. Those added costs you pass to me, the consumer. The further out the delivery, the more it costs.

This is the contango, the futures curve slopes upward. It’s the normal state for most commodities.

Now, what is backwardation?

Well, lets say I want those 1,000 barrels delivered today.

You tell me that the price is $62 per barrel.

What if I want the delivery in June?

Well you tell me that for that it costs $60.

But why is it cheaper for a later delivery? We just said that this operation has added costs so it goes against our idea on the contango scenario. Because right now the supply is tight and everyone needs oil IMMEDIATELY. The premium to have it is now, since there’s not much going around. Nobody’s paying that storage premium, and on top of that, the market is discounting future delivery because it expects the supply crunch to ease. This is backwardation, the curve slopes downward.

So now back to our hyperliquid contract. Why is it paying so much negative funding?

Well, first things first, we have this little thing that apparently no one looks at in the crypto world, that is called documentation.

If we go to the deployer’s (tradexyz) documentation of this contract, we find that the WTIOIL Oracle is currently the CLK6 futures contract, which is the Crude Oil front-month futures contract.

But we won’t be trading the May contract forever right? It has to roll to the next contract which is supposed to happen between April 8-14. After the roll, it will track the June contract which is the CLM6 contract that is currently trading around $86.56.

Now, how is the rolling of the contract done? This neat little thing called the documentation once again has the answer.

Now you can see that the rolling dates are presented in the Nth business day, which varies from month to month.

So for our current situation it translates to:

Since we are in backwardation (June’s contract is trading at lower price than front-month price) we have baked into the perpetual contract an automatic price drop each day from today until April 14th. The market has a CERTAIN expectation at what price our contract should be trading.

Given that expectation, the market is already discounting the current front-month contract price for that of the June contracts. Obviously the market isn’t waiting for the exact second to trade at new prices. This means that we’re trading at a sticky discount to the front-month (CLK6) price.

It’s sticky because there’s no longer an incentive to push price towards the current front-month contract as that will be replaced in a matter of days. So that stickiness is making the funding really really negative.

Now can you arb this to make money? Well, let’s do some back of the napkin maphs. This is where I could mess things up but let’s try not to.

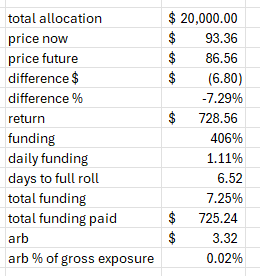

Lets say you short the hyperliquid perp at current price (93.362) and long the June contract at (86.56) each for $10,000. We know that they will trade close together on the 14th, so we have a basis to collect $6.8, which amounts to a hypothetical $729 return from the pure convergence.

However we have 406% funding to pay, lets again assume it stays the same and we will be paying 1.11% a day for that exposure. That will be a total of 156.5 hours until the full roll which is about 6.52 days. Given the $10,000 HYPERLIQUID leg exposure we will pay about -$725.24 in funding and the arb is wiped out.

That trade then gets REALLY negative if we factor in fees and market impact, which I won’t even get into here.

Now there’s a few things I am too lazy (maybe) to estimate for.

The equal position size at different prices means I don’t have a completely market neutral position. This was purely used as an example, one should factor in the different prices into the sizing formula.

I assumed the full 400% annualized funding we’re seeing now. Well as the basis collapses, since hyperliquid oracle will begin adding weight to the new month contract, also will these fundings begin collapsing (or increasing towards less negative, in this case), so using the same funding reading as of now, might be a bit too conservative.

There’s other ways to look at this that might offer good potential trades, but that’s your job now, not mine innit?

I hope it clears things up as it did for me.

Disclaimer: The content and information provided by the Trading Research Hub, including all other materials, are for educational and informational purposes only and should not be considered financial advice or a recommendation to buy or sell any type of security or investment. Always conduct your own research and consult with a licensed financial professional before making any investment decisions. Trading and investing can involve significant risk of loss, and you should understand these risks before making any financial decisions.